- Record high say-on-pay failures. According to Willis Towers Watson analysis, there were 78 say-on-pay failures for companies in the Russell 3000, which is seven more than the previous high number of failures since inception.

- COVID grace period has ended. There has been a back-to-business approach to applying scrutiny to the typical key areas of focus, including poor disclosures, one-time special awards, changes to in-cycle long-term incentive awards and responsiveness (or lack thereof).

- Performance-based incentives are important. A primary issue at companies with a negative say-on-pay recommendation and a high pay-for-performance concern is the lack of performance-based attributes for most long-term incentives.

- Non-compensation issues at board level. Board diversity is now at a point where proxy advisors are recommending against votes when companies and their boards fall short of minimum diversity expectations.

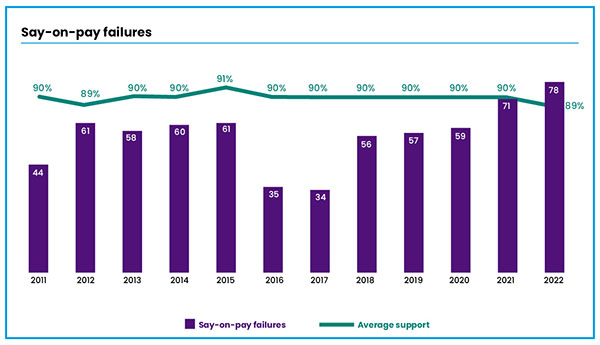

Despite a slow and rather business-as-usual start to the 2022 proxy voting season, the year-to-date outcomes have reached record territory for say-on-pay (SoP) failures.

As of Sept. 30, there were 78 SoP failures for companies in the Russell 3000, seven more than the previous highest number of failures on record since SoP inception (71 total in 2021). Not only has the overall rate of SoP proposals failing to receive majority support increased to 4%, but the average level of shareholder support has dipped below 90% for the first time in 10 years.

The percentage of companies receiving strong support (defined as greater than 90%) has declined (70% of Russell 3000), though moderate support remains the norm (86% received greater than 70% support).

The first half of the year largely reflects pay and performance ending with the 2021 calendar year, and though it seems like a distant memory at this point, 2021 saw strong total shareholder return (TSR) performance. The overall strength in the market played a role in strong performance and compensation results for fiscal 2021; however, the first nine months of 2022 have seen global economic uncertainty and enormous market volatility, yielding sustained and deep TSR losses.

For companies with non-calendar fiscal years, the perfect storm of CEO pay increases confronting bear market territory has led to record SoP failure territory. Despite statistics very similar to previous years in terms of average support, Willis Towers Watson (WTW) is observing an uptick in SoP failures, leading to a record year in that area:

Source: WTW Global Executive Compensation Analysis Team analysis

COVID-19 Pay Adjustments Drawing Heavy Scrutiny

As a refresher, in early 2020, we saw proxy advisors put a spotlight on areas that could be negatively received, with a core notion that making executives whole at the expense of broader stakeholders would be problematic. Though this seemed to be bright-line in nature, we saw a true case-by-case approach with a willingness to examine company-provided disclosure and the rationale of actions taken in response to COVID-19.

Fast-forward to 2022, we are now seeing a back-to-business approach to applying scrutiny to the typical key areas of focus, including poor disclosures, one-time special awards, changes to in-cycle long-term incentive awards and responsiveness (or lack thereof).

From WTW analysis of companies with a negative recommendation and a high pay-for-performance concern from Institutional Shareholder Services (ISS), companies with a lackluster performance that continued COVID-19 pay program adjustments without strong and detailed rationale are being called out.

As WTW predicted during a June webcast, proxy advisors and institutional investors have tightened pay scrutiny. Though there is an understanding that continuing uncertainty abounds (e.g., a potential recession, inflation concerns), there is also the expectation that companies have established guiding governance principles to move forward through the chaos.

Furthermore, the expectation is that compensation committees are using the principles to move away from the era of COVID-19 adjustments and getting back to business when it comes to pay for performance.

Performance-Based Incentives Are Important

A primary issue at companies with a negative SoP recommendation and a high pay-for-performance concern is the lack of performance-based attributes for most long-term incentives.

While this stands as a legacy issue for proxy advisors and investors alike, shareholders have returned to advocating for more performance-based incentives. This is particularly true when we’ve seen examples of special retention awards, which have been heavily scrutinized absent a strong performance-based structure with supporting rationale providing a clear linkage to the underlying issues.

While this continues as an area of heavy focus, we have seen companies with prior SoP issues work to implement new performance-based compensation (the most common program change at 42% of companies that failed SoP in 2021).

SoP Responsiveness

SoP responsiveness, especially in the face of prior year low support, continues to be a hot button issue for proxy advisors. This responsiveness is demonstrated via shareholder engagement, where companies can hear concerns directly from shareholders and further explain the compensation program’s overarching narrative in a compelling way.

Companies that do not take this engagement opportunity seriously will see ongoing proxy advisor scrutiny around SoP.

Named Executive Officer Pay Is Also Important

While ISS policy places the quantitative pay-for-performance focus squarely on CEO pay, we are seeing qualitative concerns around named executive officer (NEO) pay increasingly being raised. In cases where CEO pay is not an issue, some companies have received a negative ISS vote recommendation. Typical areas of focus for NEOs have included overall magnitude of pay and the performance-based nature of long-term incentives (or a lack thereof).

Non-Compensation-Related Issues Regarding Board Members

WTW has observed non-pay-related issues leading to nominating and governance committee withhold vote recommendations. Board diversity is now at a point where proxy advisors are recommending against votes when companies and their boards fall short of minimum diversity expectations.

WTW has also seen instances of this listed as a concern for compensation committee members with a withhold recommendation at companies with a negative SoP recommendation.

Overall, while pay for performance continues to be the largest concern for companies, responsiveness and performance-based pay design also demand attention.

In addition to monitoring the ongoing stock market volatility, focusing on compensation discussion and analysis disclosure to provide background and rationale can proactively mitigate concerns the proxy advisors and investors might otherwise have.

Editor’s Note: Additional Content

For more information and resources related to this article see the pages below, which offer quick access to all WorldatWork content on these topics: