- Final rules. The Securities and Exchange Commission adopted final rules for implementing the pay versus performance (PVP) requirement in the Dodd-Frank Act, which included a measure of “realizable pay” that includes the change in equity award fair values from one period to the next until the date of vesting.

- A new ask. What will make this new disclosure requirement so unique is that, except in limited circumstances (e.g., cash-settled awards, modified awards), companies have not been in the habit of revaluing their equity awards after the initial date of grant.

- Monte Carlo simulation model. Grant date fair values for relative total shareholder return awards are prepared using a Monte Carlo simulation model. This same model will be required for PVP valuation purposes until the end of the performance measurement period.

- Act quickly. Valuations for prior measurement dates should be prepared now to reduce the burden after year-end. These earlier valuations will also allow companies to establish processes to prepare the valuations at year-end.

The Securities and Exchange Commission (SEC) on Aug. 25 adopted final rules implementing the pay versus performance (PVP) requirement in the Dodd-Frank Act.

The final rules adopted a measure of “realizable pay” that includes the change in equity award fair values from one period to the next until the date of vesting. This was a significant departure from the proposed rules that would have required only reporting the value of equity vested for any given year, which would have been more akin to the W-2 values recognized by an executive for the year.

The main takeaway is that there is a lot of work to be done in a relatively short period of time, when many of the people who will be preparing these valuations are already busy with other year-end calculations.

What will make this new disclosure requirement so unique is that, except in limited circumstances (e.g., cash-settled awards, modified awards), companies have not been in the habit of revaluing their equity awards after the initial date of grant.

For corporate financial statement and proxy summary compensation table (SCT) reporting purposes, Accounting Standards Codification Topic No. 718 (ASC 718) requires stock-settled equity awards to be valued at the grant date. The resulting fair value creates a fixed amount of expense to be recognized and a fixed value to be captured in the SCT; therefore, valuations are prepared only once for most awards.

The new PVP rules will require companies to revalue outstanding equity awards through the date of vesting. This creates a number of new and unexpected challenges:

- The number of valuations required each year to be prepared by internal or external valuation resources will significantly increase.

- In-flight valuation of stock option awards will be required to reflect changes in assumptions that consider current fiscal year economic conditions and how much the options are in or out-of-the-money.

- In-flight valuation of relative total shareholder return (RTSR) awards will be required to reflect changes in assumptions that consider current fiscal year economic conditions and actual TSR performance for the company and peers to date.

- Other market-condition awards (e.g., stock price hurdle vesting) will face similar challenges. Companies will be required to disclose changes in valuation assumptions between the grant date and the PVP measurement date.

- For non-market-condition awards (e.g., awards subject to conditions tied to financial or non-financial goals), while complex valuation models will not be required, internal alignment will be needed on updated probability achievement factors and a shared understanding around the disclosure of this information in a new way.

Let’s look at some of the specific implications for stock option and RTSR awards, which are the awards that most frequently require measurement using valuation models.

Stock Options

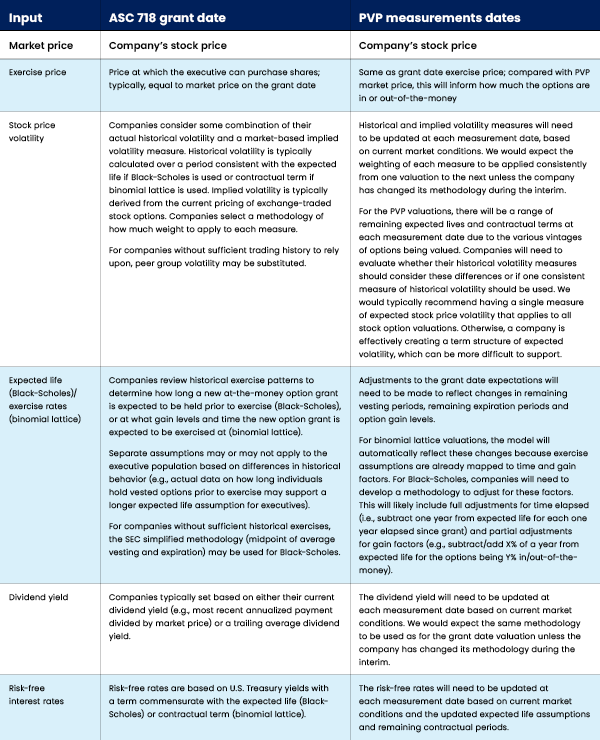

Grant date fair values for stock options are primarily prepared using either Black-Scholes or binomial lattice pricing models, with Black-Scholes being far and away the most commonly used model. We would expect companies to utilize a consistent model for PVP valuation purposes. Let’s look at the inputs (Figure 1).

Relative Total Shareholder Return Awards

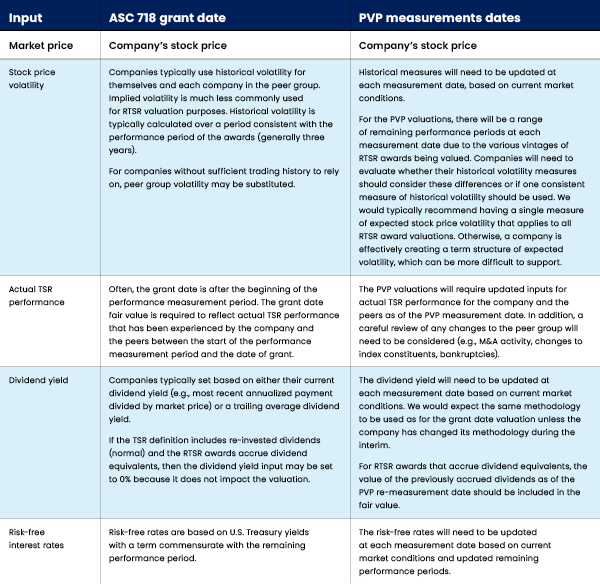

Grant date fair values for RTSR awards are prepared using a Monte Carlo simulation model. This same model will be required for PVP valuation purposes until the end of the performance measurement period. At that date, the actual relative TSR performance and the current market price will be the basis for the fair value. Let’s look at the Monte Carlo inputs (Figure 2).

Given the significant number of valuations that potentially need to be prepared, Willis Towers Watson strongly suggests starting to figure out who will be able to perform these analyses and how they will be done, as soon as possible.

A finite amount of time will be available to perform these calculations after year-end and at a time when the valuation resources are already busy working on other things, including valuations of new grants for the current year.

Valuations for prior measurement dates should be prepared now to reduce the burden after year-end. These earlier valuations will also allow companies to establish processes to prepare the valuations at year-end.

Editor’s Note: Additional Content

For more information and resources related to this article see the pages below, which offer quick access to all WorldatWork content on these topics: