- Halfway home in proxy season. At the midway point of 2023 proxy season, investors’ views on executive compensation suggest there will be less say-on-pay failures than there were in 2022.

- A pay-for-performance disconnect persists. Pay-for-performance disconnects remain the primary issue most investors and their advisors cite when voting against say-on-pay resolutions and pay outcomes are likely driving some of the reduced opposition for say-on-pay this year.

- Guidelines are likely to be updated in 2024. It’s likely investors and proxy advisers will assess the lay of the pay-versus-performance (PVP) land in 2023 and update their guidelines for 2024 to formally incorporate PVP assessments.

As the midway point of proxy voting season in the U.S. nears, investors’ views on compensation, as measured by say-on-pay vote outcomes, provide some mixed messages compared to historical outcomes. In 2022, WTW observed a record number of failed say-on-pay votes among Russell 3000 companies.

Results in 2023 suggest we’ll likely see far fewer failures, as opposition rates appear to be decreasing.

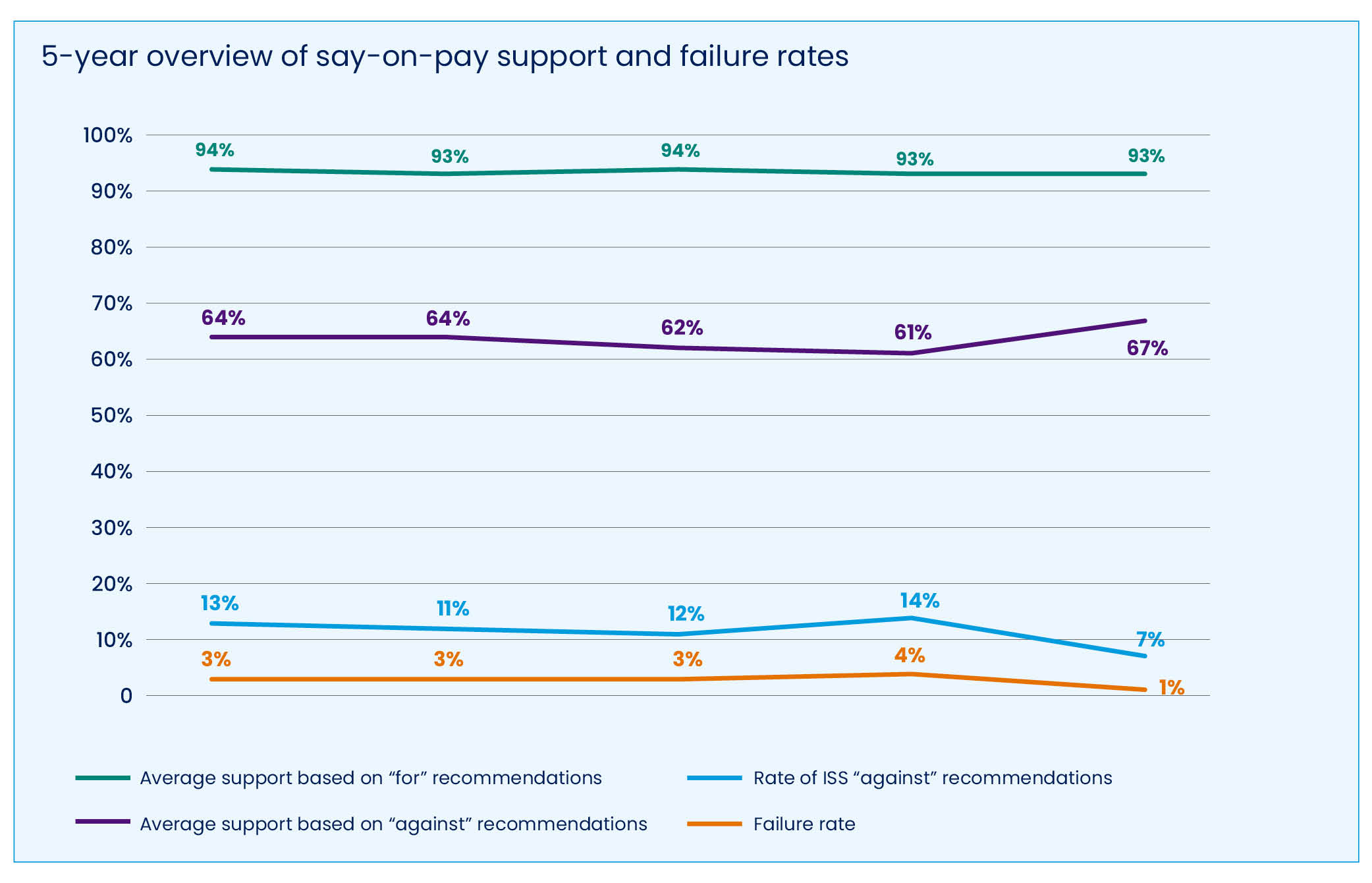

On the one hand, 2023 say-on-pay outcomes appear to be holding fairly steady. Average say-on-pay support continues to trend around 90%, with negative recommendations from proxy adviser Institutional Shareholder Services (ISS) having a 20 to 30 percentage point downward impact on outcomes.

However, as shown in graph below, the rate of ISS “no” recommendations for say-on-pay and the overall failure rate has dropped considerably so far in 2023. The 1% failure rate is derived from six failed votes observed to date, which is markedly below the 13 and 22 failed votes observed at a similar time in the proxy season in 2022 and 2021, respectively.

Source: WTW’s Global Executive Compensation Analysis Team. ISS recommendations confirmed using ISS’s Governance Analytics.

A Disconnect with Pay-for-Performance

Pay-for-performance disconnects remain the primary issue most investors and their advisers cite when voting against say-on-pay resolutions and pay outcomes are likely driving some of the reduced opposition for say-on-pay this year.

Annual bonus payouts in 2022 remained above target at the median (123% of target) but were lower than in 2021 (148% of target). Most notably, 35% of payouts in 2021 were above 170% of target, but this has dropped significantly so far in WTW’s 2022 data, with only one-fifth of companies (20%) paying bonuses over 170% of target in 2022.

Meanwhile, payouts under long-term incentive plans have held steady and generally matched shareholder return performance, owing to the underlying equity-based nature of these awards. Average payouts were slightly up relative to 2021 (117% versus 115% of target on average), suggesting companies performed well relative to their long-term strategies set in 2020.

It will be interesting to see if the early trend of less say-on-pay opposition continues to play out in the 2023 proxy season. Historically, WTW has tracked a reversion to the mean when all outcomes are ultimately tallied.

Looking Ahead

As proxy season continues, WTW will also be keeping an eye on any emerging issues as they relate to say-on-pay evaluation. A key focus will be whether the new pay-versus-performance (PVP) disclosures will materially change the way investors and their advisers review the issue.

ISS has noted that PVP may be a qualitative consideration in arriving at say-on-pay voting recommendations, although we have yet to see any real evidence so far this year. It’s likely investors and proxy advisers will assess the lay of the PVP land in 2023 and update their guidelines for 2024 to formally incorporate PVP assessments.

As organizations review their own pay practices in conjunction with say-on-pay outcomes, they should continue to monitor voting guideline updates from their major investors and the proxy advisers to stay ahead of potential issues. Engagement can also help in this regard.

Organizations should also reflect on the common reasons for say-on-pay failures and determine if these present risk areas. If so, think about engagement and appropriate disclosures that may be required ahead of any say-on-pay entanglements.

Editor’s Note: Additional Content

For more information and resources related to this article see the pages below, which offer quick access to all WorldatWork content on these topics: